Learn about our Making Work Supports Work project.

Access to secure and affordable health insurance is critical for all Americans. In the public debate, children’s coverage has received particular attention and support. But access to health care for parents is a key predictor of access to health care for children. To help inform the national debate on how to improve the health care system, this fact sheet examines current gaps in parents’ access to health coverage, looks at the patchwork of policies that exists across the states, and argues that a national approach is needed.

What the Research Says

The health insurance status of parents has important implications for their children’s health. When parents are covered, children are more apt to enroll in public health insurance programs and regularly access health care. Insured parents are also healthier parents. Parents without health insurance may forego regular care, and the resulting illnesses can impede their ability to care for their children. Routine illnesses can also threaten parents’ job security and financial stability. For parents without adequate insurance, the medical expenses associated with a serious illness can lead to financial devastation. In recent years, health care costs have become a major source of debt in the United States and a leading cause of bankruptcy.

Despite the importance of health insurance, millions of parents go without coverage. One third of all Americans under age 65 lacked health insurance during at least some part of the last two years. The present-day economic climate is expanding the ranks of the uninsured. A recent analysis found that roughly 14,000 Americans lose coverage every day, and a Congressional Budget Office report predicts that the number of uninsured will reach 54 million by 2019.

The Current Landscape

Private Health Coverage

The decline in private health coverage in recent years is at the root of the growing number of uninsured. While employer-sponsored health insurance continues to be Americans’ main source of coverage, recent trends have shown a steady erosion of employer-based benefits that has far outstripped the expansion of public health programs.

- In 2000, nearly 70 percent of Americans under 65 had employer-sponsored health insurance. By 2007, the percentage had dropped to 63 percent – with coverage reaching 3 million fewer people, even while the under 65 population rose by 16 million.

- For employees at the lower end of the pay scale, benefits such as employer-sponsored insurance are even harder to find. Among workers in the bottom fifth of the wage scale, fewer than half have employer-sponsored coverage.

Private sector alternatives to employer-sponsored coverage are often prohibitively expensive.

- Nearly half of those with private non-group insurance reported spending more than 10 percent of their income on premiums and out of pocket medical expenses, according to a recent study.

- Fewer than five percent of Americans are covered by private non-group plans.

Public Health Coverage

Millions more Americans would be uninsured without Medicaid and the Children’s Health Insurance Program (CHIP). Together these public health insurance programs cover more than 50 million children and (nonelderly) adults. Medicaid and CHIP are supported through a combination of federal and state funds, and states set eligibility criteria for the programs within federal parameters. Some states also have additional state-funded programs.

There have been significant efforts to expand coverage for children in recent years.

- In more than 40 states, public coverage is available to children living in families with income up to at least 200 percent of the federal poverty line – about $44,000 a year for a family of four.

- The 2009 reauthorization of CHIP provides states with increased funding to cover more children, along with incentives to raise children’s eligibility limits to 300 percent of poverty; in some states, limits are already above that level.

Access to coverage for parents, however, is significantly more limited and uneven.

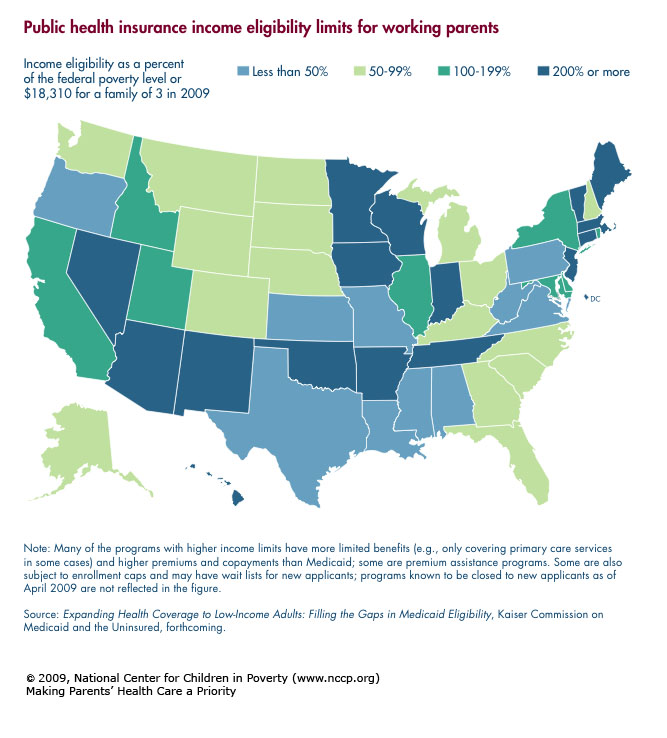

- Only a third of states have public health insurance programs open to parents with income up to at least 200 percent of the federal poverty level – the minimum level of income families need to get by.

- Moreover, many of these programs have more limited benefits and higher premiums and copayments than Medicaid. Some, for example, only cover primary care services; others are premium assistance programs. Some programs are also subject to enrollment caps and may have wait lists for new applicants.

- The 2009 CHIP reauthorization makes it even more difficult for states to expand parents’ coverage by prohibiting new CHIP waivers to cover adults.

- Finally, more than half of the states still have income limits for parents’ public health insurance that are below the poverty level, and in 10 states, the limit is less than half of the poverty level (see map).

The result is a patchwork of state policies that leaves millions of low-wage working parents without access to health insurance. Notably, childless adults and noncustodial parents have even less access to coverage.

Selected State Efforts to Expand Public Coverage for Parents

Experiences in some of the states that have worked to expand parents’ coverage provide insight into the difficulty of such efforts without greater federal support. Three examples are below.

Illinois

In 2006, Illinois became the first state to offer public health insurance to children regardless of household income, though premiums are substantial at higher income levels. But efforts to expand coverage to parents have been less successful. After failing to enact a program to cover all adults in 2007, the governor, by administrative order, raised the public health insurance income limit for parents from 185 to 400 percent of poverty. This move led to a taxpayer lawsuit, and the limit was returned to 185 percent of poverty.

Source: Bouman, John, Sargent Shriver National Center on Poverty Law. June 5, 2008 and April 29, 2009. Personal communication.

New Mexico

New Mexico also has made strides in increasing children’s access to coverage: CHIP is available up to 235 percent of poverty and Premium Assistance for Kids is available to children under age 12 and their siblings, regardless of household income. A program offering coverage to parents with income up to 400 percent of poverty was also enacted with a CHIP waiver, but despite cost-sharing provisions and limited benefits, enrollment in the program outstripped funding. A wait list for new applicants left parents facing a public health insurance income limit far below the poverty level, though with CHIP reauthorization, an increase in funds has recently allowed the state to start processing applications again.

Sources: Stauffer, Anne, New Mexico Voices for Children. Oct. 15, 2008 and April 29, 2009. Personal communication; Insure New Mexico! Solutions. (accessed April 29, 2009).

Massachusetts

The only state in the country to successfully pass legislation that aims to cover all individuals, including all parents, is Massachusetts. In 2006, Massachusetts enacted a mandate that virtually everyone in the state become insured. A central component of the plan was expanding publicly subsidized coverage to adults and children with household income up to 300 percent of the federal poverty level through Commonwealth Care. Over the next two years, Massachusetts succeeded in achieving a more than 50 percent decline in the number of uninsured residents, with just over half of the newly insured enrolled in Commonwealth Care. Commonwealth Care is financed primarily through a federal Medicaid waiver, which was renewed in September 2008. Without that renewal, the program’s future would be in jeopardy, and even so, the cost to the state has been far more than expected, prompting concerns about the sustainability of the state’s health care reform effort.

Sources: Kaiser Commission on Medicaid and the Uninsured. 2008. Massachusetts Health Reform: Two Years Later. Washington, DC: Kaiser Family Foundation; Kaiser Commission on Medicaid and the Uninsured. 2008. States Moving Towards Comprehensive Health Care Reform. Washington, DC: Kaiser Family Foundation.

A National Approach is Needed

The bottom line is that with limited financial means and balanced budget requirements, even those states with the will to expand parents’ coverage need significant federal funding to achieve this goal. The current economic crisis makes the need for federal action even more urgent. Mounting job losses are accelerating the erosion in access to employer-based health benefits, leading growing numbers to turn to Medicaid and CHIP for coverage. At the same time, nearly half of the states have enacted or proposed cuts that would reduce enrollment in public plans or limit health care access among those enrolled – or do both. Those at risk of losing coverage include nearly 600,000 adults, mostly parents, in addition to just under 500,000 children.

The importance of quality, affordable health insurance for all individuals is clear, and to ensure the health and well being of our country’s children, coverage for parents is particularly important. President Obama has promised comprehensive health care reform that will make affordable health insurance available to all. This is a promise that is long overdue, and one we hope will be fulfilled.

Endnotes

1. See Dubay, L. & Kenney, G. 2003. Expanding Public Health Insurance to Parents. Effects on Children’s Coverage Under Medicaid. Health Sciences Research, October, 38(5): 1283-1302 and Davidoff, A.; Dubay, L.; Kenney, G.; Yemane, A. 2003. The Effect of Parents’ Insurance Coverage on Access to Care for Low-Income Children. Inquiry Excellus Health Plan, Fall, 40(3): 254-268.

2. Zelda, Cindy; Rukavina, Mark. 2007. Borrowing to Stay Healthy: How Credit Card Debt is Related to Medical Expenses. New York, NY: Demos. Also see Facts on the Cost of Health Insurance and Health Care. 2009. Washington, DC: National Coalition on Health Care.

3. Americans at Risk: One in Three Uninsured. 2009. Washington, DC: Families USA.

4. Health Care in Crisis. 2009. Washington, DC: Center for American Progress.

5. Elmendorf, Douglas W. 2009. Options for Expanding Health Insurance Coverage and Controlling Costs. Testimony before the Committee on Finance. United States Senate.

6. Gloud, Elise. 2008. The Erosion of Employer-Sponsored Health Insurance. Washington, DC: Economic Policy Institute.

8. Feder, Lester; Whelan, Ellen-Marie. 2008. An Unhealthy Individual Health Insurance Market. Washington, DC: Center for American Progress.

10. Ross, Donna Cohen; Caryn Marks. 2009. Challenges of Providing Health Coverage of Children and Parents in a Recession: A 50-State Update on Eligibility Rules, Enrollment and Renewal Procedures, and Cost-Sharing Practices in Medicaid and SCHIP in 2009. Washington, DC: Kaiser Commission on Medicaid and the Uninsured.

11. Programs known to be closed to new applicants as of April 2009 are not reflected in this count. Source: Expanding Health Coverage to Low-Income Adults: Filling the Gaps in Medicaid Eligibility. Forthcoming. Washington, DC: Kaiser Commission on Medicaid and the Uninsured.

12. The 2009 reauthorization of CHIP also allows states to use federal dollars to cover legal immigrant children who meet the income criteria, without waiting until at least five years after the children entered the country, while the five-year bar on immigrant parents remains in place. Source: Families USA. 2009. CHIPRA 101: Overview of the CHIP Reauthorization Legislation. Washington, DC.

13. Turning to Medicaid and SCHIP in an Economic Recession: Conversations with Recent Applicants and Enrollees. 2008. Kaiser Family Foundation.

14. A Painful Recession: States Cut Health Care Safety Net Programs. 2008. Families USA.

15. Sparer, Michael. 2009. Medicaid and the U.S. Path to National Health Insurance. The New England Journal of Medicine, 360(4): 323-5 ; Elmendorf, Douglas W. 2009. Options for Expanding Health Insurance Coverage and Controlling Costs. Testimony before the Committee on Finance. United States Senate.